As a company director, you are responsible for the financial reporting of that business.

You're responsible for the financial reporting, regardless of whether you’re the finance director or not!!!

As a company director, you are responsible for the financial reporting of that business.

You're responsible for the financial reporting, regardless of whether you’re the finance director or not!!!

Why do we have accounting rules ?

the goal is to prevent misleading reporting, ensure comparability over time and across businesses, and make sure similar transactions are treated consistently.

Who sets the accounting rules?

As the world has become more globalised, the desire to invest and trade across boarders has increased. The International Accounting Standard Board (IASB), based in London, sets a set of accounting rules (adopted by 144 countries). The accounting rules, are called International Accounting Standards (IAS) or International Financial Reporting Standards (IFRSs). They set the rules on what information

should be disclosed, how information should be presented, how assets should be valued and how profits should be measured.

Outside of the IASB, many exchanges( London Stock Exchange) set their own regulations.

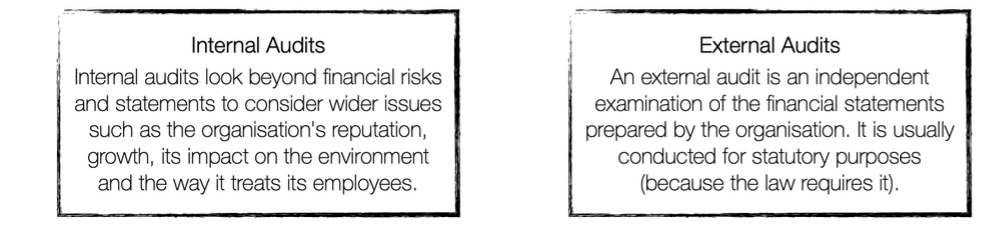

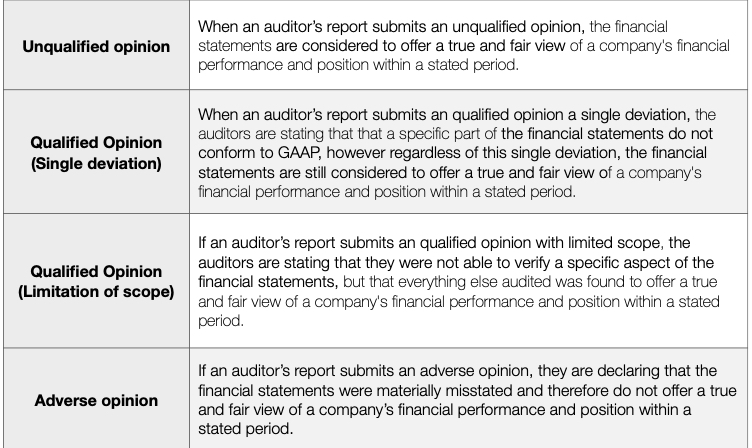

Auditor's role

independent and qualified person(s) who review the financial statements on behalf of the

shareholders and offer their opinion on whether the financial statements offers ‘a true and fair’ view

a company is exempt from auditing when it does not exceed two of the following: Annual turnover of no more than £10.2 million, assets worth no more than £5.1 million or 50 or fewer employees on average

Given the vast number of transactions, audits rely on sampling methods to make judgements. Auditors are appointed by the shareholders to review the financial statements provided by the directors.

Auditor’s Fee (this creates a potential conflict of interest on the subject of ‘independence’ because they can be lenient if they receive a huge amount)

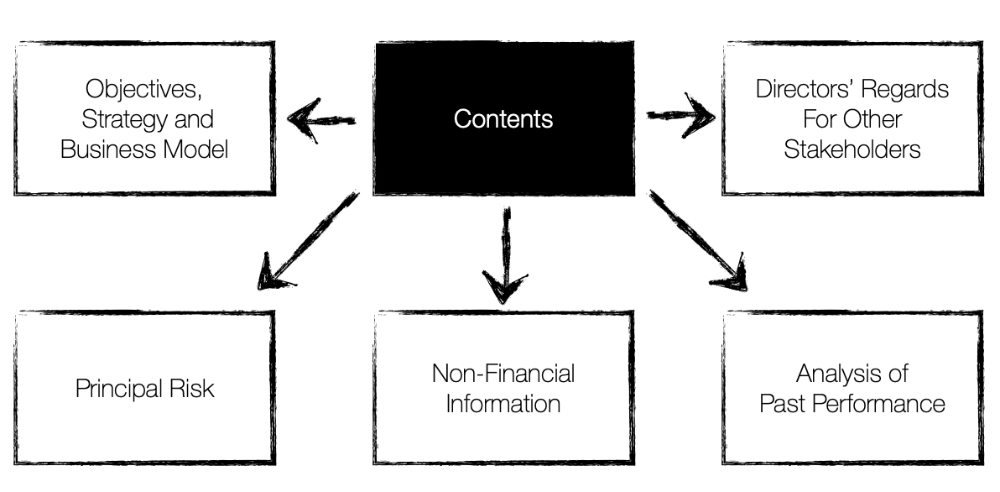

strategic report is a separately statement, which describes how the directors have discharged their duty under section 172 of the Companies Act 2006 to promote the successes of the company for the benefit of its members.

Directors of a company are required to prepare a directors’ report

at the end of each financial year. (The names of each director who served during the reporting year, A summary of the company’s trading activities A summary of future prospects...)

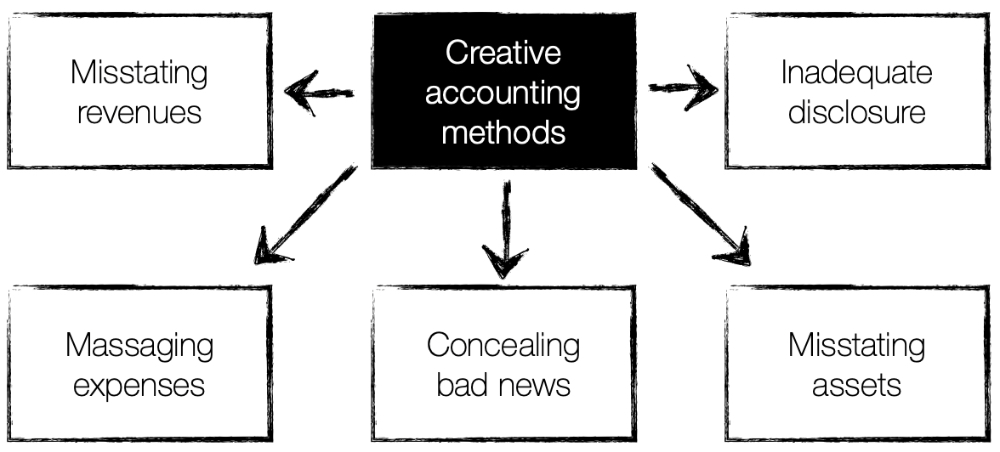

Creative accounting is intentionally misrepresenting the financial statements with the intention of misleading the users.

Misstating revenues

form of creative accounting : seeks to include deferred revenue ( prepayment) intended for the next financial year in current financial statement; seeks to record artificially sales from essentially ‘fake customers’

Massaging expenses

form of creative accounting : a company seeks to adopt accounting policies which move

expenses into different periods (depreciation, amortisation of intangible assets, costing inventories and use of provisions)

concealing bad news

This form of creative accounting :company directors seek conceal losses or liabilities. One way of doing this is to create a legal entity known as a special purpose entities (SPE)s, which hides the losses or liabilities,

misstating assets

form of creative accounting: stating asset values

which are higher than the fair values, recording assets that are not owed by the business or simply do not exist.

Inadequate disclose

form of creative accounting: company directors seeks to conceal information which should be disclosed either directly within the financial statement / annal report.

As a company director, you are responsible for the financial reporting of that business.

You're responsible for the financial reporting, regardless of whether you’re the finance director or not!!!

Why do we have accounting rules ?

the goal is to prevent misleading reporting, ensure comparability over time and across businesses, and make sure similar transactions are treated consistently.

Who sets the accounting rules?

As the world has become more globalised, the desire to invest and trade across boarders has increased. The International Accounting Standard Board (IASB), based in London, sets a set of accounting rules (adopted by 144 countries). The accounting rules, are called International Accounting Standards (IAS) or International Financial Reporting Standards (IFRSs). They set the rules on what information

should be disclosed, how information should be presented, how assets should be valued and how profits should be measured.

Outside of the IASB, many exchanges( London Stock Exchange) set their own regulations.

Auditor's role

independent and qualified person(s) who review the financial statements on behalf of the

shareholders and offer their opinion on whether the financial statements offers ‘a true and fair’ view

a company is exempt from auditing when it does not exceed two of the following: Annual turnover of no more than £10.2 million, assets worth no more than £5.1 million or 50 or fewer employees on average

Given the vast number of transactions, audits rely on sampling methods to make judgements. Auditors are appointed by the shareholders to review the financial statements provided by the directors.

Auditor’s Fee (this creates a potential conflict of interest on the subject of ‘independence’ because they can be lenient if they receive a huge amount)

strategic report is a separately statement, which describes how the directors have discharged their duty under section 172 of the Companies Act 2006 to promote the successes of the company for the benefit of its members.

Directors of a company are required to prepare a directors’ report

at the end of each financial year. (The names of each director who served during the reporting year, A summary of the company’s trading activities A summary of future prospects...)

Creative accounting is intentionally misrepresenting the financial statements with the intention of misleading the users.

Misstating revenues

form of creative accounting : seeks to include deferred revenue ( prepayment) intended for the next financial year in current financial statement; seeks to record artificially sales from essentially ‘fake customers’

Massaging expenses

form of creative accounting : a company seeks to adopt accounting policies which move

expenses into different periods (depreciation, amortisation of intangible assets, costing inventories and use of provisions)

concealing bad news

This form of creative accounting :company directors seek conceal losses or liabilities. One way of doing this is to create a legal entity known as a special purpose entities (SPE)s, which hides the losses or liabilities,

misstating assets

form of creative accounting: stating asset values

which are higher than the fair values, recording assets that are not owed by the business or simply do not exist.

Inadequate disclose

form of creative accounting: company directors seeks to conceal information which should be disclosed either directly within the financial statement / annal report.