International Trade: Exchange of capital, goods, and services across international borders or territories.

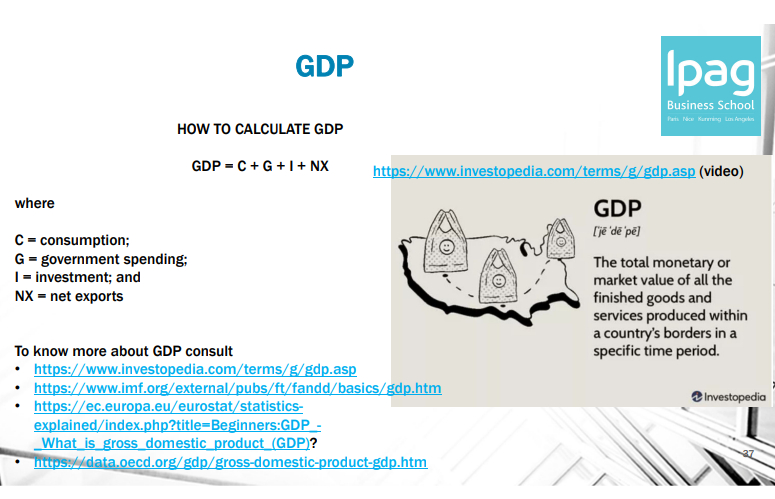

GDP: Gross Domestic Product.

Export and Import: Goods and services sold to and bought from other countries.

FDI: Foreign Direct Investment.

International Trade: Exchange of capital, goods, and services across international borders or territories.

GDP: Gross Domestic Product.

Export and Import: Goods and services sold to and bought from other countries.

FDI: Foreign Direct Investment.

Increasing international trade is crucial to the continuance of globalisation.

Some international economic organisations, such as the World Trade Organization (WTO), were formed to smoothen and justify the process of trade between countries of different economic standings. These organizations work to facilitate and grow international trade.

Historical Milestones and Trends in International Trade Growth (1953-2015)

From 1953 to 2015, international trade experienced remarkable growth marked by several historical milestones. The post-World War II era saw a significant boom due to economic reconstruction and the establishing institutions like the General Agreement on Tariffs and Trade (GATT) in 1947, which promoted trade liberalization. The 1970s were characterized by oil shocks that slowed trade growth, followed by the 1980s and 1990s, which saw technological advancements in transportation and communication and the rise of globalization. The World Trade Organization (WTO) creation in 1995 further facilitated global trade by reducing trade barriers and resolving disputes. China's accession to the WTO in 2001 was a pivotal moment, propelling it to become a major global trade player. The 2010s brought a shift towards services and digital trade, driven by e-commerce and global supply chains.

Overall, these trends reflect the dynamic evolution of international trade, influenced by technological, economic, and political changes, leading to an increasingly interconnected global economy.

The five principles of the WTO are

1. Trade without discrimination

2. Freer trade: gradually, through negotiation

3. Predictability: through binding and transparency

4. Promoting fair competition

5. Encouraging development and economic reform

Inflation • Inflation measures how much more expensive a set of goods and services have become over a certain period, usually a year. • Inflation is the rate of increase in prices over a given period of time.

‘…the process of transformation of local phenomena into global ones. It can be described as a process by which the people of the world are unified into a single society and function together. This process is a combination of economic, technological, socio-cultural and political forces’ (Croucher, 2003, p. 10).

• ‘…increasing global interconnectedness, so that events in one part of the world are affected by, have to take account of, and also influence, other parts of the world. ITiplady, 2003, p. 2). •

‘…process by which the whole world becomes a single market. This means that goods and services, capital and labor are traded on a worldwide basis, and information and the results of research flow readily between countries’ (Black, 2002).

International Trade: Exchange of capital, goods, and services across international borders or territories.

GDP: Gross Domestic Product.

Export and Import: Goods and services sold to and bought from other countries.

FDI: Foreign Direct Investment.

Increasing international trade is crucial to the continuance of globalisation.

Some international economic organisations, such as the World Trade Organization (WTO), were formed to smoothen and justify the process of trade between countries of different economic standings. These organizations work to facilitate and grow international trade.

Historical Milestones and Trends in International Trade Growth (1953-2015)

From 1953 to 2015, international trade experienced remarkable growth marked by several historical milestones. The post-World War II era saw a significant boom due to economic reconstruction and the establishing institutions like the General Agreement on Tariffs and Trade (GATT) in 1947, which promoted trade liberalization. The 1970s were characterized by oil shocks that slowed trade growth, followed by the 1980s and 1990s, which saw technological advancements in transportation and communication and the rise of globalization. The World Trade Organization (WTO) creation in 1995 further facilitated global trade by reducing trade barriers and resolving disputes. China's accession to the WTO in 2001 was a pivotal moment, propelling it to become a major global trade player. The 2010s brought a shift towards services and digital trade, driven by e-commerce and global supply chains.

Overall, these trends reflect the dynamic evolution of international trade, influenced by technological, economic, and political changes, leading to an increasingly interconnected global economy.

The five principles of the WTO are

1. Trade without discrimination

2. Freer trade: gradually, through negotiation

3. Predictability: through binding and transparency

4. Promoting fair competition

5. Encouraging development and economic reform

Inflation • Inflation measures how much more expensive a set of goods and services have become over a certain period, usually a year. • Inflation is the rate of increase in prices over a given period of time.

‘…the process of transformation of local phenomena into global ones. It can be described as a process by which the people of the world are unified into a single society and function together. This process is a combination of economic, technological, socio-cultural and political forces’ (Croucher, 2003, p. 10).

• ‘…increasing global interconnectedness, so that events in one part of the world are affected by, have to take account of, and also influence, other parts of the world. ITiplady, 2003, p. 2). •

‘…process by which the whole world becomes a single market. This means that goods and services, capital and labor are traded on a worldwide basis, and information and the results of research flow readily between countries’ (Black, 2002).