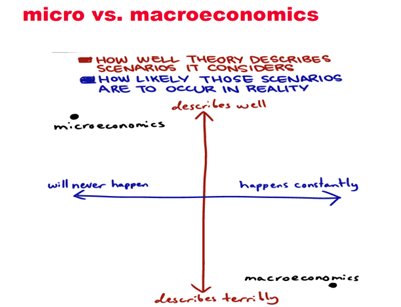

- one of the most common (and rather useless) measurement of the income of nations is the GDP

- “GDP” measures everything in short, except that which makes life worthwhile.” (Robert Kennedy, 1968)

- The GDP measures only goods and services which are traded via markets.

- Wealth is hard to measure - but can include categories such as natural capital, produced capital or human capital

SESSION 1

Définition

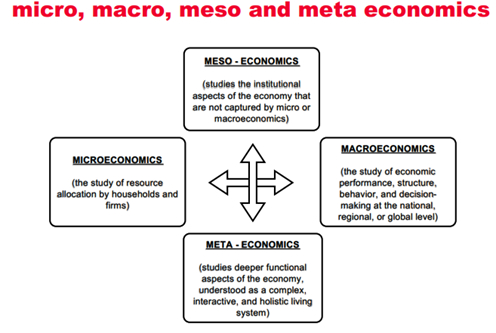

Economics

Study of mankind in the ordinary business of life, The science which studies human behaviour as a relationship between ends and scarce means which have alternative

Management

Management is to forecast, to plan, to organize, to command, to coordinate and control activities of others(Henry Fayol)

Ten principles of economics

• How people make decisions

• Principle #1: People face tradeoffs

• Principle #2: The cost of something is what you give up to get it

• Principle #3: Rational people think at the margin

• Principle #4: People respond to incentives

• How people interact

• Principle #5: Trade can make everybody better off (questionable)

• Principle #6: Markets are usually (!!!) a good way to organize market activity

• Principle #7: Governments can sometimes improve market outcomes

• How the economy as a whole works

• Principle #8: A country’s standard of living depends on its ability to produce goods and services

• Principle #9: Price rise when the government prints too much money

• Principle #10: Society faces a short-run tradeoff between inflation and unemployment

Définition

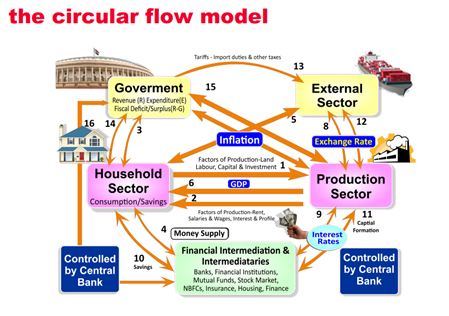

Tableau economique

by François Quesnay, a notable achievement in 18th-century economics. It envisioned the economy as a circular movement of commodities and money among many sectors

Session 2

Définition

Economic growth

increase in the capacity of an economy to produce goods and services, compared from one period of time to another. It can be measured in nominal or real terms. Traditionally measured in terms of GNP or GDP

GNP

Gross national product, the value of all finished goods and services produced by a country's citizens, both domestically and abroad

GDP

Gross domestic products, the value of the finished domestic goods and services produced within a nation's borders.

A retenir :

Economic wealth IS NOT economic income

Définition

National income

the total money created by a country's citizens and enterprises over a certain time period, and is commonly quantified as GDP or GNP.

National wealth

the accumulated worth of the nation's economic assets minus its liabilities, indicating the country's total economic resources

invention vs innovation

Définition

Invention

The act of creating something wholly new through imagination and experimenting. can be both tangible (such as a new gadget or machine) and intangible (such as a new method or process).

Innovation

Process of improving or making major modifications to current items, methods, or ideas. It can entail the use of new methods, concepts, or combinations of existing knowledge to make something better or more efficient. About applying and practicalizing ideas and technologies in ways that provide value or meet new requirements

Joseph Schumpeter

- 1883-1950

- Austrian economist

- the business cycle (1969)

- Capitalism, socialismand democracy (1942)

- defends the idea that innovation is the main source of economic growth

Types of innovation:

- New products

- Radical innovations: entirely new poducts

- Incremental innovations: enhance already existing products

- New production process

- Implementation of new or improved methods, techniques and workflows; goals are to reduce production costs, enhance product quality, and increase the efficiency and sustainability of production processes. Enables companies to gain a competitive edge, improve profitability, and meet evolving market demands

- New markets

- Innovation in outlets: finding new ways to reach customers, like selling to other countries or targeting different groups of people. It could include using new methods for selling products, like online shopping, social media advertising, or offering services like 24-hour delivery. These innovations help businesses grow by reaching more customers and improving their satisfaction (e.g., companies like Amazon or Netflix).

- New materials or resources

- Raw materials innovation involves incorporating new or alternative raw materials in the production of goods or services. This includes using renewable or recycled materials to lower production costs and reduce environmental impact, aligning with sustainability goals.

- Advanced materials, such as nanomaterials or biocompatible substances, enable breakthroughs in industries like energy, healthcare, and transportation, paving the way for novel applications and enhanced performance. These innovations not only improve efficiency and sustainability but also drive technological advancements across various sectors.

- New forms of organisations

- Innovation in production methods focuses on transforming how production processes are organized and managed. This encompasses the adoption of new forms of collaboration across the production chain, including subcontracting and partnerships. It also involves implementing innovative management practices and work organization models, such as telecommuting, flexible work schedules, and enhanced teamwork structures. These changes aim to increase efficiency, adaptability, and productivity while fostering a more dynamic and collaborative production environment

Schumpeter's Creative destruction

This creative destruction, according to Schumpeter, is necessary for economic advancement

• However, creative destruction comes with costs and difficulties for businesses and individuals, such as the closure of specific companies in a certain field

• Examples: Telemedicine in the healthcare sector; home delivery in the supermarket/retail sector

Définition

Creative destruction

the process by which an innovation replaces old products, processes, markets, and organizational forms with new ones

A retenir :

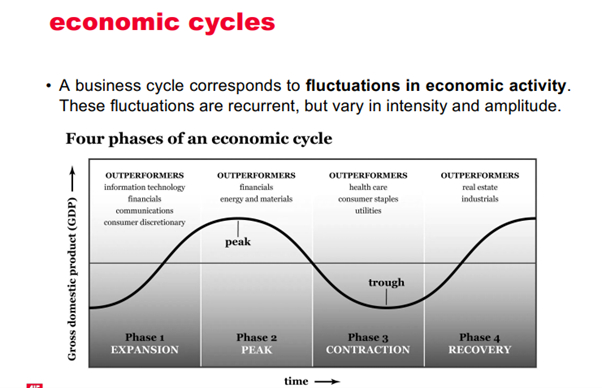

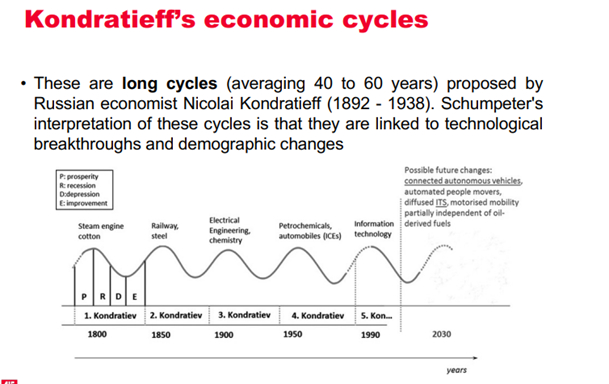

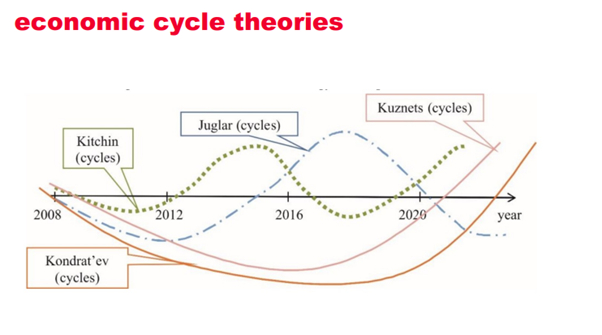

ECONOMIC CYCLE THEORIES

- Kitchin Cycles describe a business cycle that lasts between 3.5 and 5 years and is mostly driven by swings in corporate inventory levels. These cycles have growth, peak, contraction, and trough phases

- Juglar Cycles, are economic cycles lasting around 7 to 11 years and are driven by changes in capital investment and lending. These cycles include expansion, crisis or peak, recession, and recovery phases economic cycle theories

- Kuznets Cycles,are economic waves that span 15 to 25 years and are marked by heavy infrastructure investment and population transitions. These cycles reflect economic structural changes such as urbanization, technological improvements, and changes in consumer tastes

SESSION 3

Définition

Public policy

all measures taken by public authorities to respond

to social, economic and environmental problems

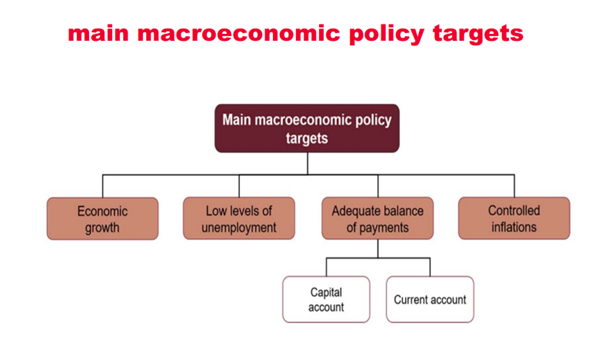

Economic policy

all measures taken by public authorities to

improve national macroeconomic performance.

- The state budget

- The money supply

- The interest rate

- Redistribution of money

- Interest rate

- Unemployment rate

- Exchange rate

- Trade balance/ Balance of payments

- Economic growth

Définition

Economic policy

the set of measures taken by public powers to improve the macroeconomic performance of nations

Fiscal policy

name given to government policies which seek to influence government revenue (taxation) and/or government expenditure

A retenir :

changes in G(government spending) or T(axation)

•Budget deficit T < G

•Budget surplus T > G

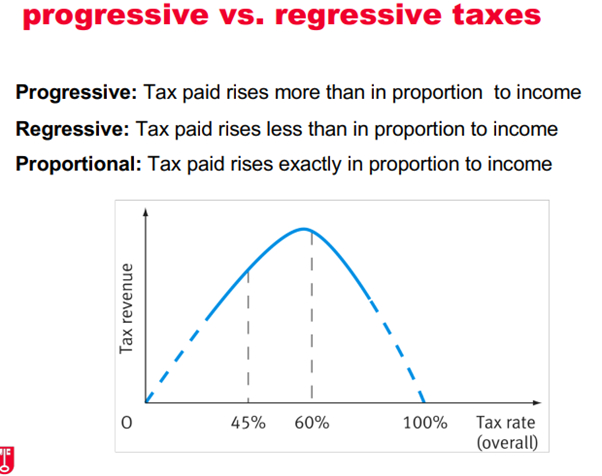

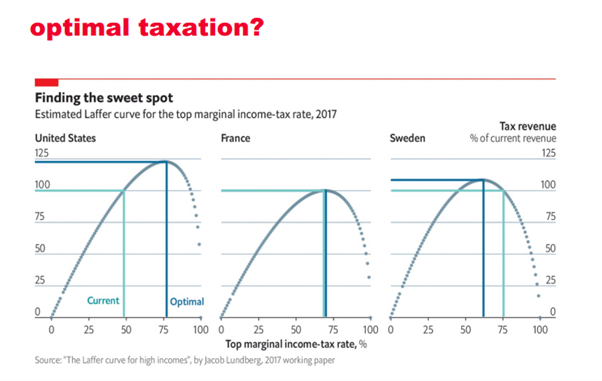

Balanced budget T = G Forms of taxation:

•Direct taxes (income tax; inheritance tax, corporate tax)

•Indirect (VAT, customs and excise duties)

•Social (security) contributions

Définition

Monetairy policy

the attempt by government to manipulate the supply of, or demand for, money in order to achieve specify objectives.

A retenir :

Changes of the rate of interest has an impact on the economy

•Savings

•Borrowings

•Discretionary expenditure

•Exchange rate

Définition

Expansionary monetary policy

increase in money supply and/or reduction in rate of interest

Contractionary monetary

policy: decrease in money supply and/or increase in rate of interest

Définition

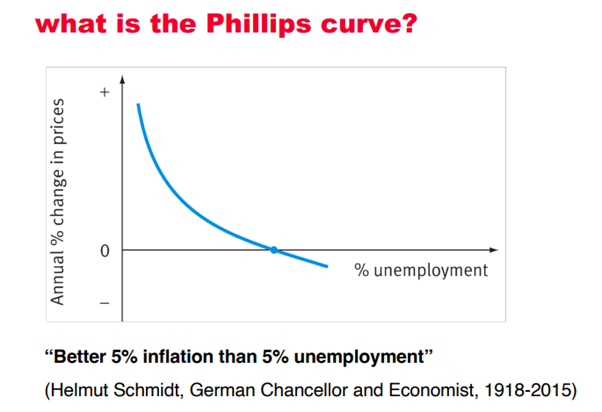

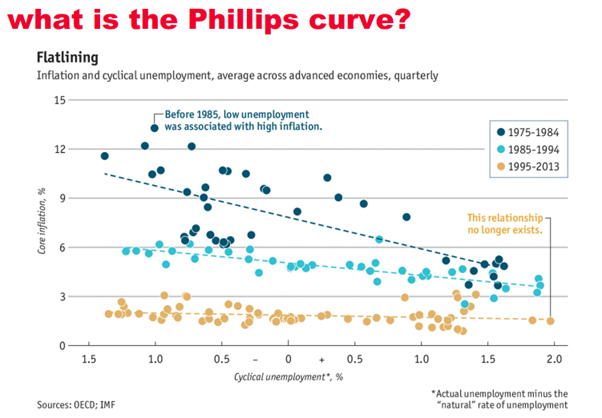

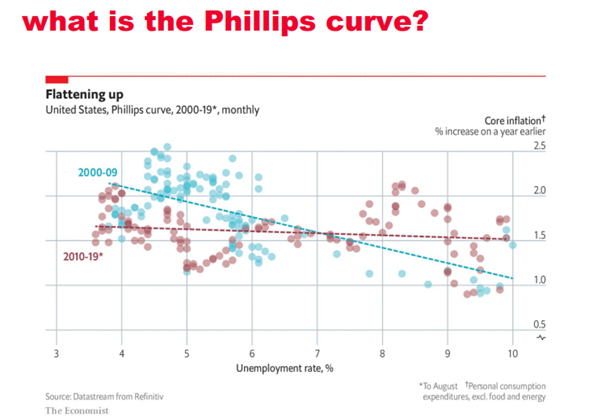

Phillips curve

The **Phillips Curve** shows the inverse relationship between inflation and unemployment: when unemployment is low, inflation tends to be high, and when unemployment is high, inflation tends to be low.

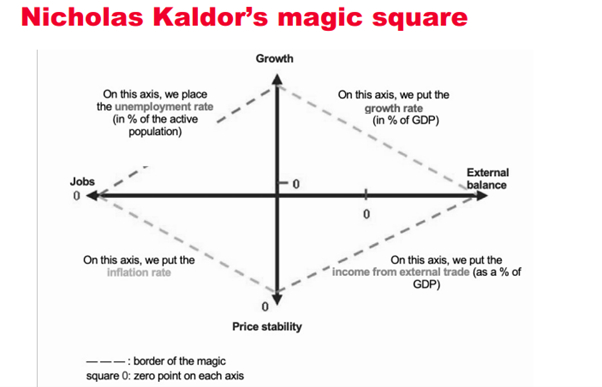

The Balance of Payments (BOP) keeps track of all money coming in and going out of a country. It has three main parts:

- Current Account: Shows trade in goods (like oil), services (like travel), income from investments, and money transfers (like aid).

- Capital Account: Records things like buying land or debt forgiveness.

- Financial Account: Tracks investments, such as buying factories or stocks.

A Balancing Item fixes any differences or mistakes in the accounts.

Myths vs. Reality about Adam Smith and Karl Marx:

- Adam Smith:

- Myth: He founded economic theory.

- Reality: He summarized existing knowledge at the time.

- Myth: He believed the “invisible hand” automatically regulates markets.

- Reality: He only mentioned it three times, in a different context.

- Myth: He was against government.

- Reality: He thought government protects the rich from the poor.

- Myth: He supported free markets without limits.

- Reality: He believed business people often harm the public for profit.

- Myth: He opposed progressive taxation.

- Reality: He supported the rich paying more in taxes.

- Myth: He thought the division of labor is always good.

- Reality: He warned it can make workers dull and uncreative.

- Myth: He said people are always self-interested.

- Reality: He believed people care about others' happiness too.

- Karl Marx:

- Myth: He wrote about communism in Capital.

- Reality: He didn't focus on communism there.

- Myth: He was always against capitalism.

- Reality: He admired what capitalists achieved, like global trade.

- Paradox: Marx saw capitalism as a form of exploitation, similar to feudalism, leading to his call for a communist revolution.

In short, both Smith and Marx had more nuanced views than commonly believed.

SESSION 4

Définition

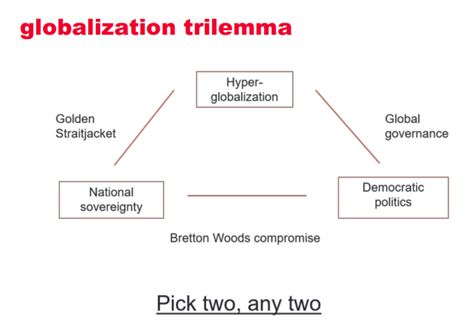

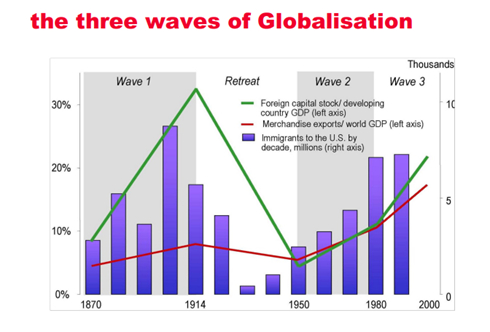

Globalization

a historical stage of accelerated expansion of market capitalism, like the one experienced in the 19th century with the industrial revolution....and has led to a recombining of the economic and social forces on a new territorial dimension“

A retenir :

Types

• Economic globalization

• Common ecological constraints

• Cultural globalization

• Globalization of communication

• Political globalization

Définition

Protectionism

an economic policy where a country tries to protect its own industries by limiting imports from other countries.

A retenir :

· Tariff measures: For a country, this may involve imposing customs duties taxes on imported products to make them to make them more expensive on its domestic market

· Non-tariff measures can also be implemented quantitative limits such as quotas, or standards sanitary, technical or environmental environmental standards

Fathers of protectionism:

• Alexander Hamilton (1757-1804)

• Advocated for protectionism, emphasizing that tariffs and governmental support were essential to foster domestic industries and reduce dependence on foreign imports

• Friedrich List (1789-1846)

• Advocated protectionist measures for infant industries, to protect the national market in the short and medium term, to enable free trade in the long term

• Donald Trump based his ideas of protectionism on the ideas of List!

Définition

DHL global connectedness report

measures a country’s global trade and logistics connectivity, based on trade volume, infrastructure, and logistics performance. A higher rank means better international connections.

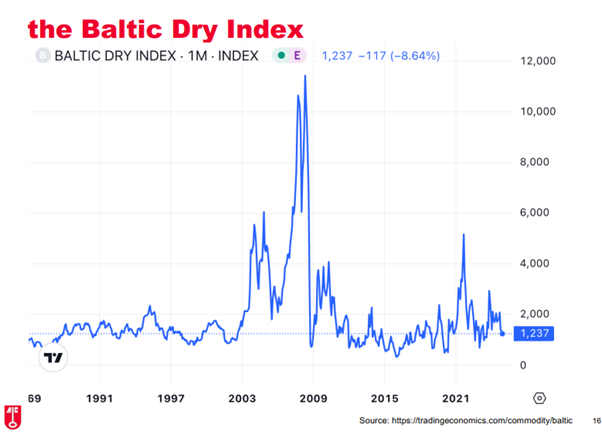

Définition

Baltic Dry Index (BDI)

measures the cost of shipping raw materials (like coal, iron ore, and grain) by sea. It tracks the rates for different types of cargo ships, reflecting global demand for shipping and economic activity. A higher BDI indicates higher demand and economic growth, while a lower BDI suggests weaker demand.

A retenir :

A shrinking world: countries are easier and easier to travel to, shorter distances and travel time

A retenir :

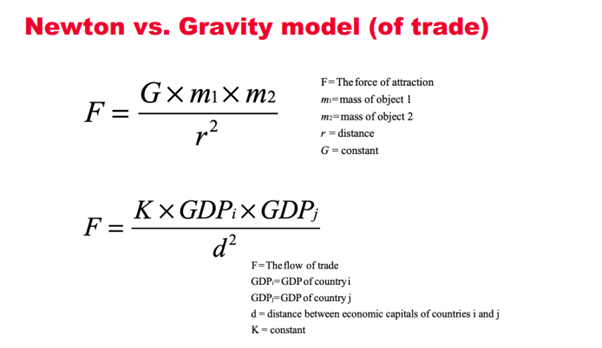

Distance impacts trade, -distance = +trade

· Cultural differences

· administrative

· geographic

· Economic

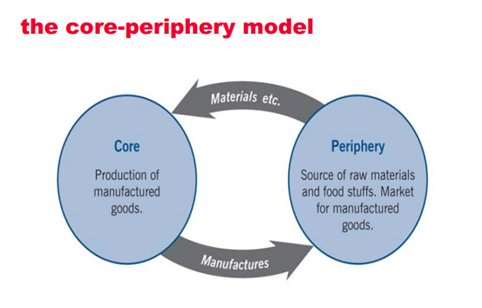

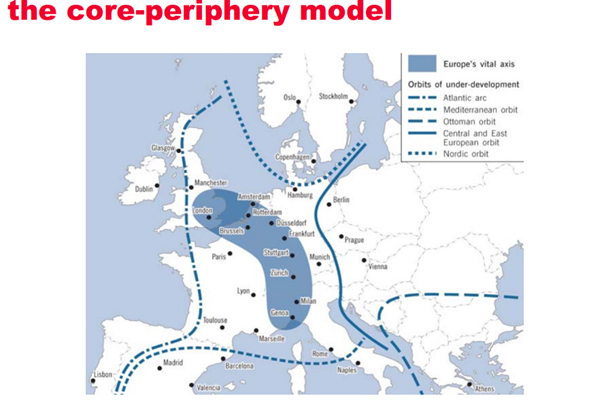

The **Core-Periphery Model** explains the uneven development between regions within a country or globally. In this model: - **Core** regions are economically advanced, with high levels of industrialization, wealth, and resources. - **Periphery** regions are less developed, often relying on raw materials and labor, and may have lower economic growth. The model suggests that the core benefits from more investment and resources, while the periphery remains dependent on the core for growth, leading to regional inequality.

A retenir :

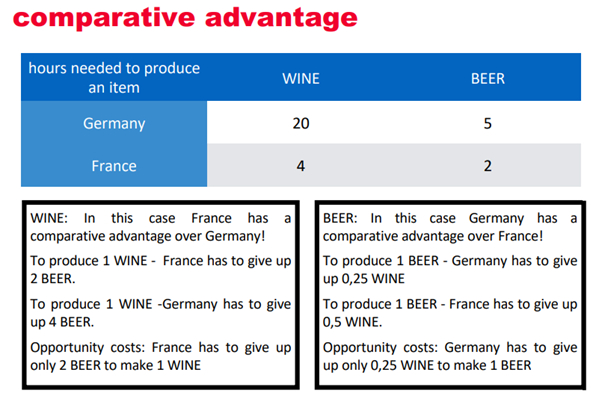

Absolute vs Comparative Advantage:

- Absolute Advantage: A country has an absolute advantage if it can produce a good more efficiently (at a lower cost) than another country. Each country should specialize in producing what it does best to maximize returns.

- Comparative Advantage: Even if a country doesn't have an absolute advantage, it should specialize in producing the good where it has the smallest disadvantage, benefiting both countries through trade.

COMPARATIVE ADVANTAGE:

In real life David Ricardo’s theory is rather useless

• David Ricardo listed several assumptions of his model and states if only ONE of them does not hold, you cannot apply his model

Assumptions:

• All humans are clones (homogeneity of labor)

• Each and everybody has a job (full employment)

• Everything is produced only by labor (no machines, no raw materials)

• Citizens of both countries have the exact same taste for products

• All countries trade on the barter system (money does not exist)

• No innovation is possible

• Capital and labor are perfectly mobile within each country

• Capital and labor are immobile between countries

• There are no costs of transportation • The planet consist only of two countries (not more!!!!)

A retenir :

The Heckscher-Ohlin-Samuelson model:

• Each country should specialise in production using the production factors it has in abundance.

• The production factors considered are: labour, capital, and land.

• However, each country should import the goods for which it has the least production factors

• Specialisation is based on the resources each country has for each factor.